Oil futures volatility and the economy

Image: Pixabay

The drone strike on Saudi Arabia’s oil infrastructure has highlighted the fragile and interconnected relationship between crude oil supply and the global economy, with new research bringing these economic ties into greater focus.

“We shouldn’t underestimate the importance of geopolitical events in the oil market, as it has the power to impend the stability of our financial world,” says University of Technology Sydney Finance researcher Dr Christina Sklibosios Nikitopoulos.

“On 16 September 2019 the oil market witnessed one of the highest intraday moves, with a 15% increase in Brent oil prices and an 14.7% increase in US WTI oil futures. Oil price spikes are seen as a recession barometer, but it is not just price but also volatility that matters,” she says.

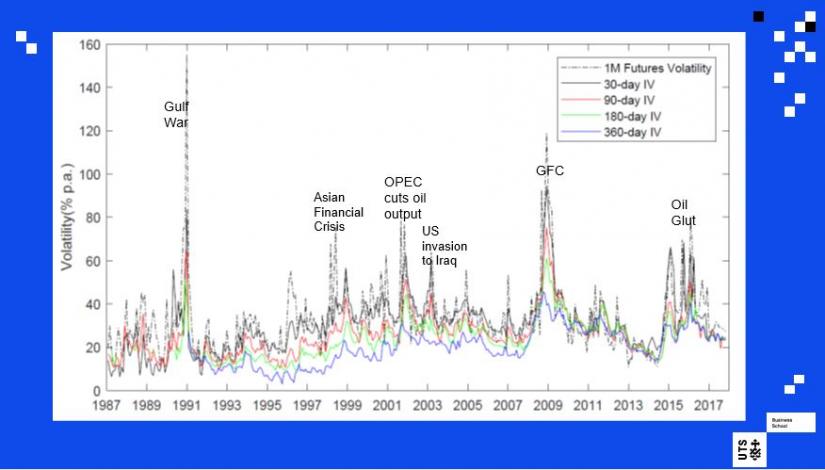

In a recently released paper, Dr Nikitopoulos, with colleagues Dr Boda Kang from Lacima Group, and Finance Professor Marcel Prokopczuk from Leibniz University Hannover, examined the connections between oil futures volatility and the global economy.

Oil markets should be the focus of global discussions by policy makers, not just individual decisions from the US Commodity Futures Trading Commission or OPEC.

Dr Christina Sklibosios Nikitopoulos

They looked at 30 years of data to discover economic determinants of oil futures volatility over the short, medium and long-term. These included oil-sector variables, financial variables and macroeconomic conditions.

The research revealed how deeply integrated crude oil markets have become with financial markets.

The crude oil derivatives market has provided a rollercoaster of volatility for market participants.

“Investors increasingly regard commodities as an alternative asset class to equities or bonds, and crude oil derivatives are the most actively traded commodity,” says Dr Nikitopoulos.

Oil futures started trading in 1983, and options in 1986, and since then the market has experienced explosive growth. Daily trading volume has leapt from 21,997 contracts in 2012 to 1.6 million in 2016 and this week surpassed 2 million.

“Our study highlighted the importance of risk premiums in this market, and revealed that credit spreads play a significant role in determining short-term and medium-term variation in oil futures prices,” she says.

In the bond market, term structure – the rate at which people can borrow or lend over different periods, is seen as an important economic signal – whether the yield term is up signalling growth or down signalling recession.

Term structures in oil markets can be seen in a similar light, where contango (where the futures price of a commodity is higher than the spot price) or backwardation (where the spot or cash price of a commodity is higher than the forward price) provide an economic signal.

Dr Nikitopoulos says the expected supply shortfall following the drone strike would cause oil futures markets to remain in backwardation for a while.

The researchers found that along with hedging pressure and VIX (an equities market volatility index) after 2004 (the beginning of the financialisation of the commodity markets) credit spreads, industrial production and the US dollar index, were all drivers of short-term volatility.

“This supports the notion of volatility spill-overs between equity and commodity markets, which has strengthened in the past 10 years, says Dr Nikitopoulos.

“It also supports the notion that oil volatility acts as a recession barometer, and fears about the impact of oil shocks on financial stability are justified,” she says.

Medium-term volatility was consistently related to open interest (a measure of trading activity) and credit spreads, while oil sector variables such as inventory and consumption had a measurable impact after 2004 due to structural changes in the economy and the oil sector.

Dr Nikitopoulos argues that because oil futures volatility is a product of interaction between the oil-sector and the economy, there is a need for mutually consistent policies.

“Oil markets should be the focus of global discussions by policy makers, not just individual decisions from the US Commodity Futures Trading Commission or OPEC,” she says.

“Crude oil futures volatility plays an important role in the global economy and has significant implications for market participants – from oil producers and institutional investors, to traders and market regulators.

“And while the US economy can manage this most recent oil shock with its own shale oil production and opening of strategic reserves, it is global markets like Australia that suffer the most through an increase in fuel costs,” she says.